Gap Between First-Time Buyer and Repeat Buyer Risk Continues to Widen

As Agency first-time buyer mortgages get riskier, the gap between fist-time buyer mortgage risk and repeat buyer mortgage risk continues to get wider, according to data released on Monday by the American Enterprise Institute (AEI)’s International Center on Housing Risk.

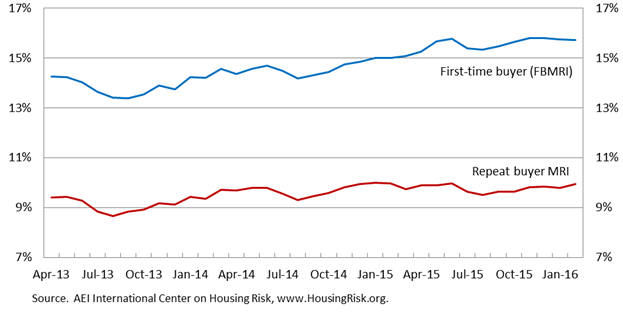

As Agency first-time buyer mortgages get riskier, the gap between fist-time buyer mortgage risk and repeat buyer mortgage risk continues to get wider, according to data released on Monday by the American Enterprise Institute (AEI)’s International Center on Housing Risk.The Agency First-Time Buyer Mortgage Risk Index (FBMRI) rose year-over-year by 0.7 percentage points in February up to 15.7 percent, meaning that 15.7 percent of Agency mortgages would default if they experienced economic stress comparable to the 2007-08 financial crisis, according to AEI.

Meanwhile, the Agency FBMRI is now 5-3/4 percentage points higher than the mortgage risk index for repeat homebuyers, up 5 percentage points over-the-year, AEI reported. First-time homebuyers have been responsible for essentially all of the year-over-year increase in the composite National Mortgage Risk Index (NMRI) since early 2015, which is a further indicator that the gap is growing larger for risk on first-time buyer mortgages and repeat buyer mortgages.

“The gap between first-time buyer and repeat buyer mortgage risk levels now stands at 5.79 percentage points compared to 5.03 and 4.85 percentage points in February 2015 and 2014 respectively,” said Ed Pinto, codirector of AEI’s International Center on Housing Risk. “Given the long running seller’s market, risk layering works to artificially push up prices, particularly for entry-level buyers; the result is a pernicious wealth transfer from the buyers to sellers of these homes.”

“The gap between first-time buyer and repeat buyer mortgage risk levels now stands at 5.79 percentage points compared to 5.03 and 4.85 percentage points in February 2015 and 2014 respectively,” said Ed Pinto, codirector of AEI’s International Center on Housing Risk. “Given the long running seller’s market, risk layering works to artificially push up prices, particularly for entry-level buyers; the result is a pernicious wealth transfer from the buyers to sellers of these homes.”Risk layering is largely responsible for the widening of the gap between risk in first-time homebuyers and repeat homebuyers. In February 2016, 20 percent of first-time buyers had a combined LTV ratio of 95 percent of higher and 97 percent of them had a 30-year term. The combination of a low down payment and slow amortization means that barring substantial home price appreciation, this group of homeowners will have very little equity for many years.

Also, according to AEI, one-fifth of first-time buyers had a FICO score lower than 660, which is the traditional definition of subprime mortgages, and one-fourth of them had debt-to-income ratios of higher than the 43 percent set by the Qualified Mortgage rule. By comparison, repeat homebuyers had a much smaller share of buyers with CLTVs higher than 95 percent and a much smaller share of borrowers with FICO scores below 660.

In February 2016, the median first-time buyer with an Agency mortgage made a down payment of 3.5 percent, which calculates to about $8,600, and the median FICO score for first-time buyers with Agency mortgages was 707—only slightly below the median for all individuals in the U.S. with a FICO score (713).

“The typical first-time buyer these days has a relatively low credit score and puts little money down.” said Stephen Oliner, codirector of AEI’s International Center on Housing Risk. “These facts make clear that mortgage credit isn't tight.”

http://www.dsnews.com/news/03-21-2016/gap-between-first-time-buyer-and-repeat-buyer-risk-continues-to-widen

No comments:

Post a Comment