The Impact of HAMP on GSE-Backed Loans

The government’s Home Affordable Modification Program (HAMP) is scheduled to expire at the end of this year. Launched in February 2009, the program was originally set to expire at the end of 2013 but has been extended twice.

The government’s Home Affordable Modification Program (HAMP) is scheduled to expire at the end of this year. Launched in February 2009, the program was originally set to expire at the end of 2013 but has been extended twice.In seven years, HAMP has completed 2.3 million homeowner assistance actions for 1.8 million families. How many of those homeowner assistance actions were completed on loans backed by Fannie Mae and Freddie Mac, and what percentage of them are still active?

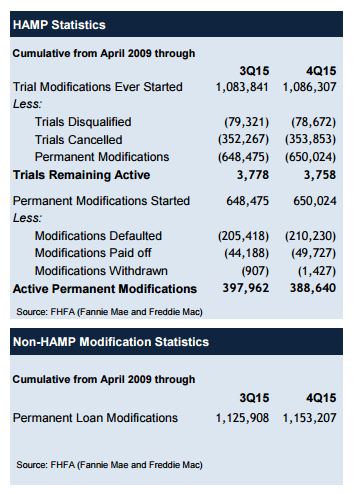

According to FHFA’s foreclosure prevention report for the fourth quarter of 2015 released on Thursday, from April 2009 until the end of Q4 2015, approximately 1.086 million homeowners with GSE-backed loans were granted HAMP trial mods. Out of those, 650,024 received permanent modifications.

Of the slightly more than 650,000 permanent HAMP mods started on GSE-backed loans over the last seven years, 388,640 of them (about 60 percent) were active as of the end of the fourth quarter in 2015, according to FHFA. Approximately 210,000 of them (32 percent) had defaulted, and about 50,000 (8 percent) had paid their loans off in full. A small share of them (1,427, or less than 1 percent) had withdrawn from their HAMP modification, according to FHFA.

As of the end of the fourth quarter, a total of 3,758 homeowners were in a trial HAMP modification period, according to FHFA.

By comparison, a total of 1.153 million homeowners received modifications on GSE-backed loans through the GSEs’ proprietary modification programs from April 2009 until the end of Q4 2015, including the 27,299 completed during Q4. Non-HAMP modifications accounted for 91 percent of all the permanent modifications completed on GSE-backed loans during the fourth quarter. The numbers reported by FHFA showed that GSE-backed loans modified through HAMP had consistently performed better throughout the last seven years than those that have received non-HAMP modifications.

By comparison, a total of 1.153 million homeowners received modifications on GSE-backed loans through the GSEs’ proprietary modification programs from April 2009 until the end of Q4 2015, including the 27,299 completed during Q4. Non-HAMP modifications accounted for 91 percent of all the permanent modifications completed on GSE-backed loans during the fourth quarter. The numbers reported by FHFA showed that GSE-backed loans modified through HAMP had consistently performed better throughout the last seven years than those that have received non-HAMP modifications.The GSEs completed 47,769 foreclosure prevention solutions during Q4, bringing the total of distressed homeowners helped through a foreclosure prevention action to 3.643 million since the start of the conservatorships in September 2008. More than three million of those foreclosure prevention actions have been home retention solutions. By comparison, there were 25,096 foreclosure sales completed during the fourth quarter, approximately half the number of foreclosure prevention actions completed during the same time.

A decline in foreclosures over the last four years has also meant a decline in the number of foreclosure prevention actions, which have dropped from 541,000 in 2012 to 448,000 in 2013 to 307,000 in 2014 to 232,000 in 2015.

At a time when many housing fundamentals are normalizing or returning to pre-crisis levels, Treasury officially began winding down MHA in early March when it issued its first set of guidelines to servicers for MHA program termination in the form of Supplemental Directive (SD) 16-02.

Click here to view the entire foreclosure prevention report for Q4 2015.

http://www.dsnews.com/news/03-24-2016/the-impact-of-hamp-on-gse-backed-loans