New FHA Changes Streamline Loss Mitigation Protocols

The Federal Housing Administration (FHA) released a Mortgagee Letter containing new procedures to strengthen the process mortgage servicers use to help struggling families avoid foreclosure and remain in their homes, according to an announcement from The Federal Housing Administration (FHA). The release says FHA is streamlining its loss mitigation protocols that servicers must use when evaluating and deploying ‘home retention options,’ foreclosure alternatives that allow delinquent borrowers to retain their home. The release also says that mortgagees must implement the policies set forth in the Mortgagee Letter no later than December 1, 2016.

The release notes that FHA’s revised procedures streamlines the process servicers use to engage borrowers, particularly when evaluating them for the FHA-Home Affordable Modification Program (FHA-HAMP). It states that these changes will decrease the number of steps a servicer and borrower need to follow in order to resolve a delinquency and enter into a loss mitigation home retention product. In addition, it also says that FHA is eliminating particular obstacles that will allow servicers greater flexibility for evaluating an unemployed borrower’s financial condition and special forbearance agreements.

Specifically, FHA reports that they will:

- Require servicers to convert successful 3-month trial modifications into permanent modifications within 60 days instead of the average four-to-six months.

- Allow borrowers with three missed mortgage payments to qualify for a partial claim to bring their arrearages current versus the previous four-month minimum.

- End the traditional stand-alone Loan Modification option so borrowers can access the FHA-HAMP option, with its greater payment relief, sooner.

- Eliminate the minimum 12-month delinquency term to qualify for FHA’s special forbearance option. This will allow servicers extend this option to unemployed households sooner in their delinquency.

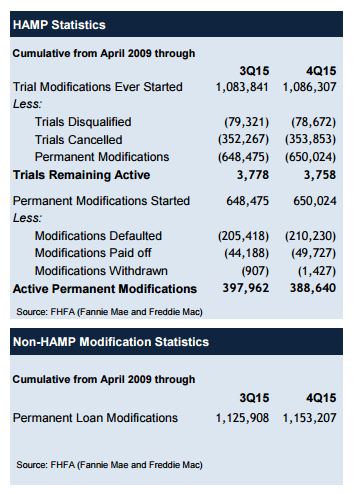

FHA’s Loss Mitigation Program was created in 1996 to reduce the economic impact to the Mutual Mortgage Insurance Fund, and subsequently has resulted in options available to Mortgagees in order to aid borrowers in avoiding foreclosure, when possible. The FHA states that the evolution of their loss mitigation guidance has also led to improved consumer engagement, the streamlining of FHA’s PreForeclosure Sale option, and a new loan modification by which Mortgagees provide borrowers with a more sustainable monthly mortgage payment.

Additionally, HAMP was created in 2009, at the height of the economic crisis. The FHA shares that these efforts combined with those of other federal regulators (U.S. Department of Veteran Affairs, U.S. Department of Treasury, etc.) have helped stabilize the nation’s housing market as well as demonstrate that a mortgage modification is an effective loss mitigation home retention option.